Luxury dealers offer payment plans because they transform a six-figure sticker price into a monthly figure that fits a buyer's actual cash flow. This financing structure, formally called an installment payment plan, removes the single biggest barrier to closing a sale on a high-end vehicle: the psychological weight of paying everything at once. Brands like BMW, Mercedes-Benz, and Porsche have long used captive financing arms to support this model, and the strategy has only grown more deliberate in 2026. Understanding why luxury dealers offer payment plans reveals as much about dealer economics as it does about buyer psychology.

Why do luxury dealers offer payment plans?

Payment plans exist because affordability is a timing problem, not just a price problem. A buyer who earns $300,000 a year may still prefer not to wire $120,000 in a single transaction. Aligning payment schedules with a buyer's salary cycles or quarterly bonus payouts closes sales that would otherwise stall, without requiring the dealer to cut the price.

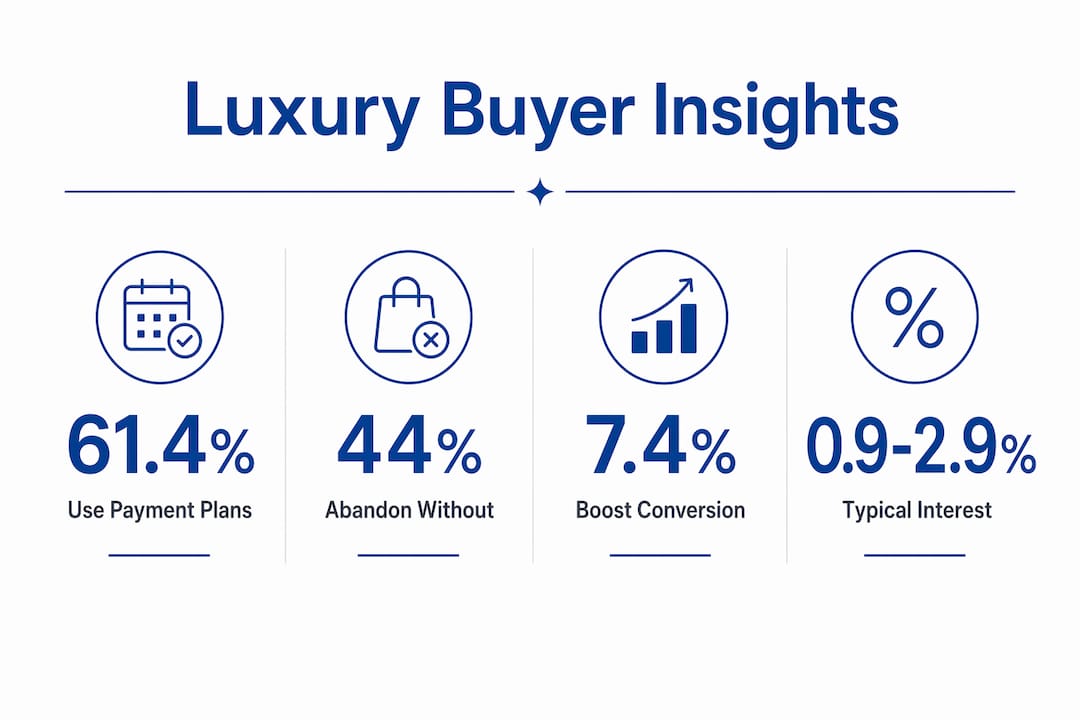

Dealers also benefit directly from the structure. Flexible installment options boost conversion rates by 7.4% and revenue by 12%. That is a meaningful lift on vehicles already carrying high margins. The math makes payment plans a business decision, not just a customer service gesture.

How payment plans improve affordability for luxury car buyers

Payment plans work by spreading the vehicle's total cost across a fixed number of months, keeping each individual payment within a buyer's comfortable range. The total price does not change. What changes is when the money leaves the buyer's account. That distinction matters enormously for buyers managing multiple investments, properties, or business cash flows simultaneously.

The psychological effect is equally real. A $95,000 Mercedes-Benz GLE presented as $1,600 per month feels like a different decision than a $95,000 lump sum. Dealers use this reframing deliberately. Sticker shock is reduced by breaking the price into installments, which preserves the buyer's sense of control without requiring a discount.

Key buyer benefits include:

- Preserved liquidity. Cash stays available for investments, emergencies, or other purchases.

- Predictable budgeting. Fixed monthly payments are easier to plan around than a single large outflow.

- No forced liquidation. Buyers avoid selling stocks or assets at an inconvenient time to fund a car purchase.

- Faster decision-making. Smaller individual payments reduce the deliberation time before signing.

Pro Tip: Ask the dealer whether the installment plan carries interest before signing. Many manufacturer-backed plans offer promotional periods at 0%, which means you pay the same total price as a cash buyer while keeping your capital free.

Research confirms that 44% of customers abandon a high-value purchase when flexible payment options are not available. For luxury dealers, that abandonment rate represents real lost revenue on vehicles priced well above the market average.

What data reveals about luxury buyers and payment plan adoption

The assumption that wealthy buyers always pay cash is outdated. 61.4% of affluent Americans earning over $100,000 annually now use buy-now-pay-later or installment services. That figure reflects a deliberate financial preference, not financial strain.

Affluent buyers use payment plans as a liquidity management tool. Keeping $100,000 invested in a portfolio earning 8% annually while making car payments at 0% interest is a straightforward financial win. High-net-worth consumers recognize this calculus, and dealers who offer installment structures capture that segment more effectively than those who do not.

The business impact on dealers is equally clear:

- Installment structures can boost average order value by 68% for premium products.

- Buyers who use payment plans tend to add more options and packages, since each upgrade adds only a small amount to the monthly figure.

- Customer retention improves when buyers feel the purchase process was financially comfortable rather than stressful.

"Payment plans signal a shift from making luxury accessible to responding to high-net-worth clients' preference for liquidity management and ease."

This cultural shift matters for dealers. Offering installment options is now a signal of sophistication, not a sign that the dealership is catering to buyers who cannot afford the vehicle outright.

How payment plans serve as a pricing and brand strategy for dealers

Payment plans are a deliberate pricing tool, not a concession. The core logic is simple: a dealer who discounts a $100,000 vehicle by $5,000 loses $5,000 in margin permanently. A dealer who offers a payment plan loses nothing on the vehicle price and may earn interest income on top.

This approach protects brand equity. Luxury brands like Bentley and Rolls-Royce guard their residual values carefully. Discounting erodes those values across the entire model line. Installment plans offer pricing flexibility that preserves brand value while still closing the sale.

Dealers use payment plans strategically in four specific ways:

- Overcome price objections without discounting. The monthly figure replaces the total price in the buyer's mental frame.

- Increase F&I revenue. Finance and insurance products attach more easily when buyers are already in an installment mindset.

- Convert cash buyers on add-ons. Even cash buyers prefer installment plans for extended warranties and service packages to protect their liquidity.

- Reduce sales friction. Buyers who feel financially comfortable close faster and negotiate less aggressively.

Pro Tip: When a dealer presents a payment plan, ask for the full amortization schedule. This shows the total cost, interest charges, and payoff date in one document. A reputable dealer provides this without hesitation.

Understanding how luxury vehicle trade-in appraisal works alongside payment plan structures gives buyers a clearer picture of their total transaction, including what their current vehicle offsets against the new purchase.

Comparing payment plans with other luxury car financing options

Luxury car buyers have four primary options: outright cash purchase, dealer installment plans, third-party auto loans, and leasing. Each serves a different financial profile.

| Financing option | Monthly cost | Builds equity | Interest risk | Best for |

|---|---|---|---|---|

| Cash purchase | None | Yes, immediately | None | Buyers with liquid assets and no investment opportunity cost |

| Dealer installment plan | Fixed, often low rate | Yes | Low to none on promo plans | Buyers prioritizing liquidity management |

| Third-party auto loan | Moderate | Yes | Moderate, varies by credit | Buyers with strong credit seeking competitive rates |

| Leasing | Lowest | No | Low | Buyers who prefer new vehicles every 2–3 years |

Leasing generally offers lower monthly payments but builds no ownership equity. Loan payments are higher in the short term but contribute to full ownership. The right choice depends on how long you plan to keep the vehicle and how you value liquidity versus equity.

Manufacturer captive financing arms, such as BMW Financial Services and Mercedes-Benz Financial Services, offer promotional rates between 0.9% and 2.9% on luxury vehicle loans. Dealer markup on interest rates is common, so arriving with a pre-approval from a bank or credit union gives you a concrete benchmark before accepting any dealer-arranged financing.

Situations where payment plans outperform other options:

- You have the cash but prefer to keep it invested.

- The dealer offers a 0% promotional period that matches your planned ownership window.

- You want to add service packages or warranties without a large upfront outlay.

- Your bonus or income arrives in irregular cycles and you want predictable monthly costs in between.

Reviewing time-saving car buying strategies before visiting a dealership helps you enter financing conversations with a clear framework rather than reacting to whatever the finance office presents.

Key Takeaways

Luxury dealers offer payment plans because installment structures protect dealer margins, remove buyer hesitation, and align with affluent consumers' preference for liquidity over lump-sum spending.

| Point | Details |

|---|---|

| Timing beats price cuts | Aligning payments to buyer cash flow closes more sales than reducing the vehicle price. |

| Affluent buyers choose installments deliberately | 61.4% of high-income Americans use installment plans as a liquidity tool, not out of necessity. |

| Dealers protect brand equity | Payment plans avoid discounting, which preserves residual values across the model line. |

| Conversion rates improve measurably | Flexible installment options increase dealer conversion rates by 7.4% and revenue by 12%. |

| Compare all options before signing | Manufacturer promotional rates, third-party loans, and leases each carry different long-term costs. |

What I've learned watching luxury buyers finance vehicles

After years of observing how high-net-worth buyers approach vehicle purchases, one pattern stands out clearly. The buyers who negotiate hardest on price are rarely the ones with the most cash. The buyers who ask the sharpest questions about payment structure are usually the ones with the most financial sophistication.

The cultural shift here is real. Paying cash for a luxury car used to signal status. Keeping your capital working and making structured payments is now the smarter move for many buyers, and the market has caught up to that reality. Dealers who understand this stop treating payment plans as a fallback for buyers who cannot afford the car. They present installment options upfront, as a feature of the purchase experience.

My practical advice: get the total cost of ownership in writing before you focus on the monthly payment. A low monthly figure stretched over 72 months can cost more than a higher payment over 48 months. The monthly number is a comfort metric. The total cost is the real one. Buyers who keep both figures in view make better decisions and feel better about them afterward.

— Allen

Explore flexible payment plans at Autovendorsfl

Autovendorsfl specializes in premium and luxury vehicles at its Fort Lauderdale location, with a hands-on approach to matching buyers with the right vehicle and the right financing structure. The team works directly with buyers to build installment plans that fit real cash flow needs, not just standard bank templates. Whether you are considering a pre-owned BMW, a certified Mercedes-Benz, or another high-end model, Autovendorsfl provides personalized guidance through every step of the financing process. Visit Autovendorsfl to explore current inventory and discuss payment plan options tailored to your situation.

FAQ

Why do luxury dealers offer payment plans instead of discounts?

Payment plans preserve the vehicle's full price and protect brand equity. Discounting reduces residual values across the model line, while installment plans close the sale without touching the sticker price.

Are payment plans for high-end vehicles only for buyers who can't pay cash?

No. Research shows 61.4% of high-income Americans use installment plans as a liquidity management strategy, keeping their capital invested rather than tied up in a vehicle.

What interest rates do luxury car payment plans typically carry?

Manufacturer captive financing arms offer promotional rates between 0.9% and 2.9% on qualifying models. Dealer markup is common, so securing a pre-approval from an outside lender before visiting the dealership gives you a useful comparison point.

How do payment plans compare to leasing a luxury car?

Leasing offers lower monthly payments but builds no ownership equity. An installment plan costs more per month but results in full ownership, which matters if you plan to keep the vehicle beyond the standard lease term.

Can a payment plan increase what I spend on a luxury vehicle?

Yes, if you are not careful. A comfortable monthly payment can make expensive add-ons feel minor, which raises the total purchase price. Always review the full amortization schedule and total cost before signing any installment agreement.