Negative equity in auto trade is defined as owing more on your car loan than the vehicle's current trade-in value. This gap is more common than most buyers realize. 29.3% of all trade-ins toward new vehicle purchases carried negative equity in Q4 2025, the highest rate since Q1 2021. The average shortfall runs around $7,200 per vehicle. That figure is not a minor rounding error. It is a real financial obstacle that shapes your next loan, your monthly payment, and your long-term budget.

What is negative equity in auto trade and why does it happen?

Negative equity, also called being "underwater" on a loan, follows a simple formula: loan payoff amount minus trade-in value equals your equity position. When that number is negative, you carry a debt gap into any trade-in transaction. Negative equity equals loan payoff minus trade-in value, and that gap does not disappear when you hand over the keys.

Several factors push buyers into this position:

- Long loan terms. Loans stretched to 72 or 84 months keep monthly payments low, but the vehicle depreciates faster than the principal drops. You stay underwater for years.

- Low or zero down payments. Starting a loan at or above the vehicle's purchase price means any depreciation immediately creates a gap.

- Rapid early depreciation. New vehicles lose a significant portion of value in the first year. A buyer who finances 100% of a new car's price is often underwater within months.

- Market shifts. Sudden drops in used car demand, fuel price changes, or model discontinuations can push trade-in values lower than expected.

- Credit-driven loan terms. Buyers with lower credit scores often receive higher loan-to-value ratios and higher interest rates, both of which deepen negative equity faster.

Pro Tip: Before you visit a dealership, pull your loan payoff amount from your lender and get an independent trade-in estimate from Kelley Blue Book or a similar valuation tool. Knowing your exact equity position before negotiations start gives you real leverage.

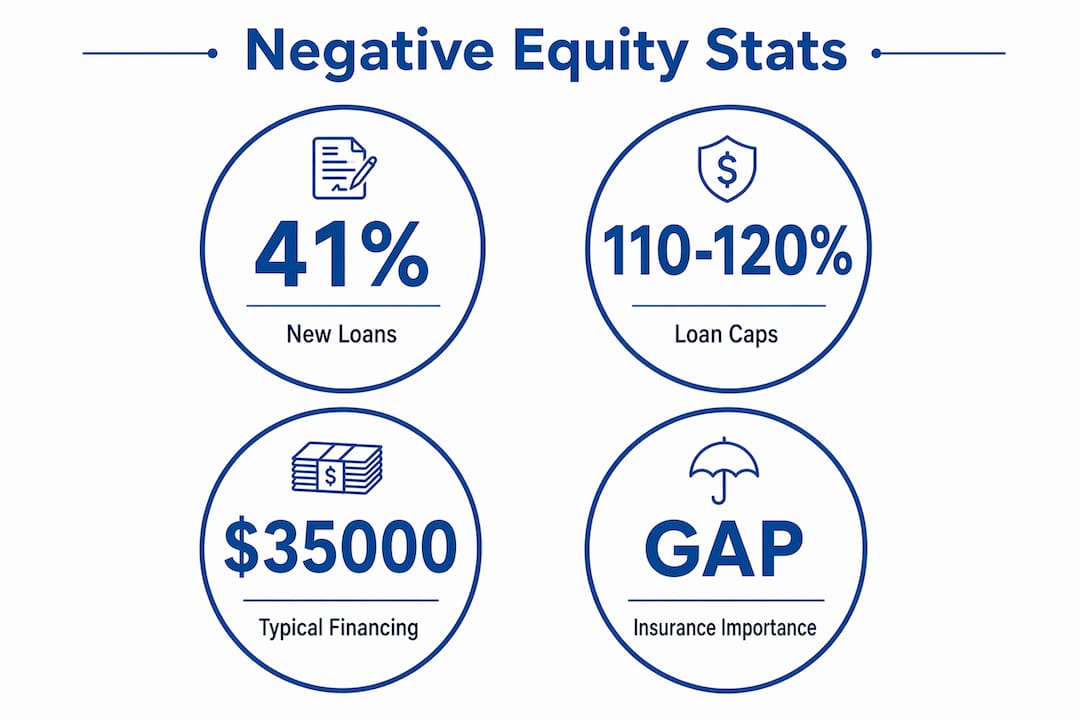

Consider a concrete example. You financed $35,000 on a vehicle two years ago with a small down payment. Today, your payoff balance is $28,000, but the trade-in value is $22,000. Your negative equity is $6,000. That $6,000 must be resolved before or during any trade-in deal.

What are the financial impacts of negative equity when trading in a car?

The financial consequences of auto trade negative equity are direct and compounding. When you trade in a vehicle with a gap between your loan balance and its value, you face two primary paths.

- Pay the difference in cash. You write a check for the gap at closing. This is the cleanest option. It costs you money upfront but prevents the debt from growing.

- Roll the negative equity into the new loan. The dealer adds your outstanding gap to the new vehicle's loan balance. Your new loan starts higher than the car's actual purchase price.

- Refinance the current vehicle. If your credit has improved, refinancing at a lower rate can reduce monthly payments and help you pay down principal faster before trading.

- Delay the trade-in. Keeping the current vehicle and making accelerated payments is often the most cost-effective path when the gap is large.

Rolling negative equity into a new loan is the most common choice, and it carries real costs. Rollover increases loan principal and interest over the full term of the new loan. If you roll $6,000 of negative equity into a new $40,000 loan at 7% over 72 months, you pay interest on $46,000 from day one. That adds hundreds of dollars in total interest costs.

The loan term problem compounds this further. Approximately 41% of new car purchases with negative equity were financed with 84-month loans. Longer terms mean slower principal reduction, which means buyers stay underwater longer and carry greater risk into their next trade-in.

GAP insurance becomes critical in this scenario. GAP insurance covers the balance difference if your vehicle is totaled and your standard insurance payout falls short of the loan balance. Without it, a total loss event could leave you paying thousands on a car you no longer own. If your new loan exceeds the vehicle's value after rollover, GAP coverage is not optional. It is a financial necessity.

One often-overlooked consequence involves taxes. Negative equity does not generate a tax credit on a trade-in. Trade-in tax credits apply only to the vehicle's actual trade-in value, not to the portion used to cover your loan gap.

How can you avoid or reduce negative equity in an auto trade?

Reducing negative equity starts before you sign your first loan. The decisions you make at purchase time determine how quickly you build or lose equity.

- Put down 20–25% upfront. Larger down payments reduce negative equity risk by starting the loan well below the vehicle's purchase price. Depreciation has less room to create a gap.

- Choose a 3–4 year loan term. Shorter terms mean faster principal reduction. Your loan balance drops in step with the vehicle's value rather than lagging behind it.

- Make extra principal payments. Paying even $50–$100 extra per month toward principal accelerates equity building significantly over a 48-month loan.

- Choose vehicles with strong resale value. Certain makes and models hold value better than others. Selecting a vehicle known for strong resale value reduces the depreciation gap over time.

- Time your trade-in carefully. Trading in a vehicle during the first two years of ownership, when depreciation is steepest, maximizes your negative equity exposure.

Pro Tip: Always negotiate the new vehicle price and your trade-in allowance as two completely separate transactions. Dealers sometimes bundle them into a monthly payment figure that obscures how much negative equity you are actually carrying into the new deal.

The comparison below shows how loan structure affects equity position over 36 months on a $35,000 vehicle:

| Loan structure | Down payment | Term | Equity position at 36 months |

|---|---|---|---|

| Minimal down, long term | $1,000 (3%) | 84 months | Likely negative |

| Standard down, mid term | $5,250 (15%) | 60 months | Near breakeven |

| Strong down, short term | $8,750 (25%) | 36 months | Likely positive |

The pattern is clear. Front-loading your financial commitment at purchase protects you at trade-in time.

What should car buyers know before trading in a car with negative equity?

Understanding the full process before you walk into a dealership prevents costly surprises. The trade-in appraisal process involves the dealer assessing your vehicle's condition, mileage, and market demand, then offering a trade-in value. That value is then applied against your loan payoff. If the payoff exceeds the value, the gap is yours to resolve.

Lenders impose loan-to-value limits that directly affect whether a rollover deal is even possible. LTV caps typically limit financing to 110–120% of the new vehicle's value. If your negative equity pushes the new loan above that ceiling, the lender may decline the deal entirely or require a large cash contribution to close. Buyers with lower credit scores face tighter LTV limits and higher interest rates, which makes large rollovers even harder to finance.

Key considerations before trading in a vehicle with negative equity:

- Get your exact payoff amount in writing from your lender before any dealer conversation. Payoff amounts change daily with accruing interest.

- Research your vehicle's trade-in value independently using Kelley Blue Book or a similar tool before the dealer appraisal.

- Understand the debt cycle risk. Rolling negative equity into new loans creates a pattern that can take years to escape. Each rollover adds to the next loan's starting balance.

- Consider whether holding is smarter. Keeping the car longer and accelerating payments is often the best path out of negative equity. Patience here pays off financially.

- Ask about leasing as an alternative. Leasing a new vehicle while paying down your current loan separately can break the rollover cycle, though it requires carrying two payments temporarily.

The car buying process rewards buyers who arrive prepared. Knowing your numbers before negotiations start puts you in control of the outcome.

Key Takeaways

Negative equity in auto trade is a manageable problem, but only when buyers understand the numbers, structure loans carefully, and resist the temptation to roll debt forward repeatedly.

| Point | Details |

|---|---|

| Definition of negative equity | Negative equity means your loan payoff exceeds your vehicle's trade-in value. |

| Prevalence in the market | 29.3% of trade-ins carried negative equity in Q4 2025, averaging around $7,200 per vehicle. |

| Rollover risk | Rolling negative equity into a new loan increases principal, interest costs, and underwater duration. |

| Prevention strategy | A 20–25% down payment and a 3–4 year loan term are the most effective ways to avoid negative equity. |

| Best exit path | Holding the current vehicle and making accelerated principal payments reduces negative equity faster than trading in. |

The rollover trap is the real danger

The part of negative equity that catches most buyers off guard is not the gap itself. It is what happens when they roll it forward. I have seen buyers carry the same $5,000 to $7,000 debt ghost through three consecutive vehicle purchases, each time convinced that a new car solves the problem. It does not. It compounds it.

The conventional wisdom says to trade in early and often to stay in a newer vehicle. That advice ignores the math. When you roll negative equity into a new loan, you are financing a debt that produces no asset. You pay interest on money that bought you nothing. Over an 84-month term, that cost is not trivial.

What actually works is less exciting but far more effective. Pay down your current loan aggressively. Make one extra payment per year. Resist the upgrade impulse until your equity position is positive. Then negotiate your trade-in and new purchase as two separate deals, because mixing them in one monthly payment is exactly how dealers obscure how much debt you are actually carrying forward.

The buyers who come out ahead treat their vehicle as a depreciating asset that requires active management, not a lifestyle accessory to upgrade on a whim. That mindset shift is worth more than any negotiation tactic.

— Allen

How Autovendorsfl supports buyers through trade-in decisions

Navigating a trade-in with negative equity requires clear information and honest guidance, not pressure. Autovendorsfl brings deep expertise in vehicle trade-in evaluations and financing options to every buyer conversation, particularly for those considering luxury vehicles where trade-in values and loan structures carry significant weight.

The team at Autovendorsfl takes a hands-on approach to understanding your current loan position, your vehicle's market value, and the financing options that make sense for your situation. Whether you are working through a gap on your current vehicle or planning a purchase that avoids one entirely, Autovendorsfl provides the personalized attention that generic dealerships rarely offer. Reach out to discuss your trade-in position before you commit to a deal.

FAQ

What does negative equity mean on a car loan?

Negative equity on a car loan means your outstanding loan balance is higher than the vehicle's current market value. The difference between those two figures is the amount you owe beyond what the car is worth.

Can you trade in a car if you have negative equity?

You can trade in a car with negative equity, but the gap must be resolved. Options include paying the difference in cash or rolling it into the new loan, which increases your new loan's starting balance and total interest cost.

How much negative equity is too much to roll over?

Lenders typically cap financing at 110–120% of a new vehicle's value. If your negative equity pushes the new loan above that threshold, the deal may require a cash contribution or may not be financeable at standard rates.

Does negative equity affect your credit score?

Negative equity itself does not directly lower your credit score. However, taking on a larger loan to cover rolled-over equity increases your debt load, which can affect your debt-to-income ratio and future borrowing capacity.

What is the fastest way to get out of negative equity?

The fastest path out of negative equity is to keep your current vehicle and make accelerated principal payments. Even modest extra monthly payments shorten the timeline significantly and reduce total interest paid.